Lightweight Aluminium Beverage Cans Market to Reach USD 35.04 Billion by 2035, Growing at a CAGR of 7.5%

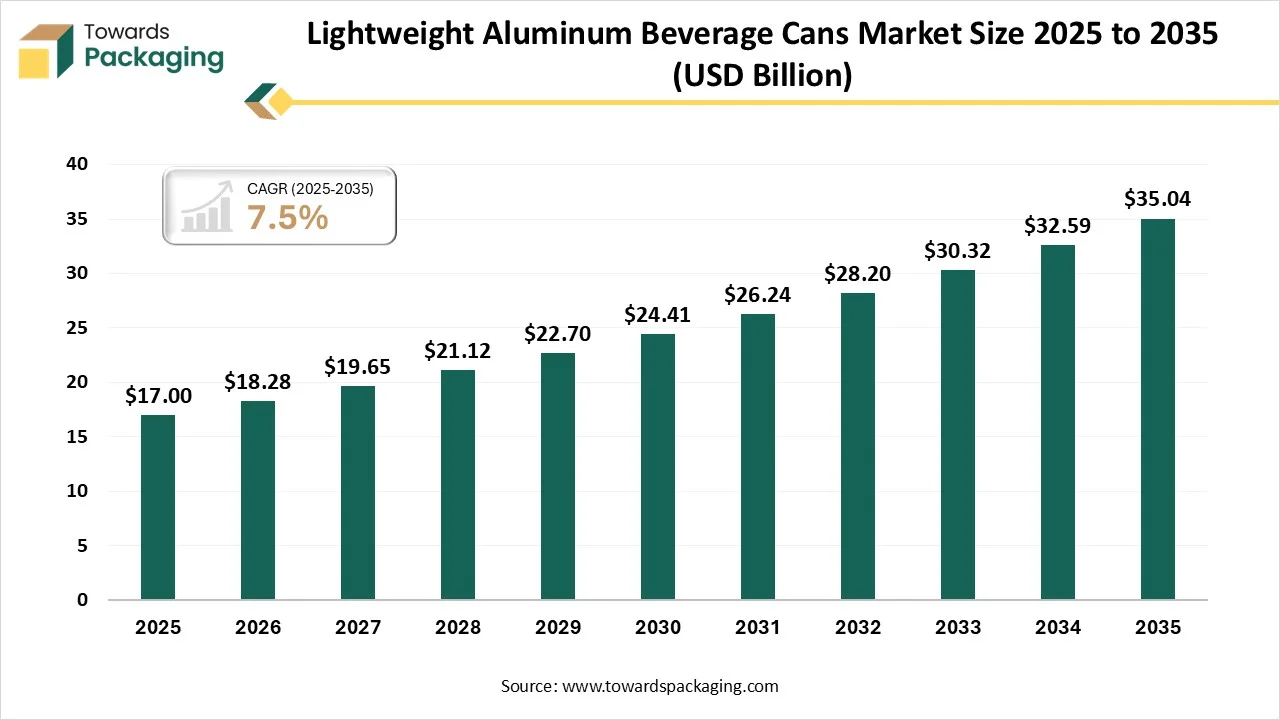

As per market analysts at Towards Packaging, the global lightweight aluminium beverage cans market is expected to grow from USD 17 billion in 2026 to nearly USD 35.04 billion by 2035, registering a CAGR of 7.5% between 2026 and 2035.

Ottawa, Feb. 24, 2026 (GLOBE NEWSWIRE) -- The global lightweight aluminium beverage cans market size reached approximately USD 17 billion in 2025, with projections suggesting it will climb to USD 35.04 billion in 2035, according to a report from Towards Packaging, a sister firm of Precedence Research.

Request Research Report Built Around Your Goals: sales@towardspackaging.com

What are Lightweight Aluminum Beverage Cans?

Lightweight aluminum beverage cans are containers engineered with thinner walls and high-strength alloys to reduce material use without compromising durability, carbonation retention, or shelf life. They are gaining strategic importance as brands pursue sustainability goals, lower transportation costs, and improved recyclability. Lightweighting also supports regulatory pressure to cut emissions, enhances supply-chain efficiency, and enables higher production volumes while maintaining product protection and visual appeal.

Private Industry Investments for Lightweight Aluminum Beverage Cans:

- Crown Holdings: The company has committed a significant portion of its R&D toward its "Twentyby30" goal of making aluminum cans 10% lighter by 2030, having already achieved a 4% reduction in standard 12 oz. can weights.

- Ball Corporation: In addition to its $290 million Nevada expansion for lightweight can production, Ball recently invested $60 million in its Sri City facility to scale operations and technical innovation for the fast-growing Indian market.

- Ardagh Group: The company has successfully refined its manufacturing processes to produce cans that are up to 10% lighter, significantly reducing material consumption and related CO2 emissions.

- Constellium: This aluminum leader is investing in the development of new, recycling-friendly alloys specifically for can ends, allowing for thinner gauges and higher recycled content without sacrificing performance.

-

Novelis: As a major supplier, Novelis is investing $2.5 billion in a new low-carbon rolling and recycling plant in Alabama to produce high-recycled-content aluminum sheets that support lightweighting efforts for global beverage brands.

What Are the Latest Key Trends in the Lightweight Aluminum Beverage Cans Market?

-

Sustainability and recycling focus:

Manufacturers are increasing the use of recycled aluminum to lower carbon footprints and meet circular economy goals. Governments and brands are prioritizing eco-friendly packaging, making lightweight cans attractive due to their high recyclability, reduced waste generation, and compliance with evolving environmental regulations.

-

Lightweighting and material efficiency:

Producers are developing thinner can walls using advanced alloys and forming technologies to reduce raw material usage without affecting strength. This lowers production and transportation costs, improves energy efficiency, and helps companies achieve emission-reduction targets across supply chains.

-

Design and technology innovation:

Brands are adopting digital printing, specialty coatings, and smart packaging features to enhance shelf appeal and consumer engagement. Lightweight cans now support premium finishes, limited-edition designs, and improved functionality, helping beverage companies differentiate products and respond quickly to changing market trends.

What is the Potential Growth Rate of the Lightweight Aluminum Beverage Cans Industry?

The lightweight aluminum beverage cans industry is expected to grow steadily through the coming decade, supported by strong demand for sustainable and material-efficient packaging. Growth is being driven by the rising consumption of energy drinks, ready-to-drink beverages, and craft products, particularly in the Asia-Pacific and North America regions.

Continuous innovations in ultra-light can designs, slim formats, and higher recycled content are improving cost efficiency and environmental performance, making lightweight aluminum cans an increasingly preferred packaging option for global beverage manufacturers.

Get All the Details in Our Solutions - Access Report Sample: https://www.towardspackaging.com/download-sample/5973

Regional Analysis:

Who is the leader in the Lightweight Aluminum Beverage Cans Market?

The Asia-Pacific region dominates the lightweight aluminum beverage cans industry due to its concentrated beverage production hubs, cost-competitive manufacturing, and strong investments in high-speed canning lines across China, India, Vietnam, and Thailand. Regional converters are prioritizing downgauging technologies to reduce metal input per unit while protecting margins amid aluminum price volatility. Multinational beverage brands are expanding localized sourcing to shorten supply chains and manage logistics costs.

China Lightweight Aluminum Beverage Cans Market Trends

China’s market is advancing through aggressive capacity rationalization and technology upgrades by major domestic and multinational can makers. Producers are deploying high-speed, precision forming lines to achieve further metal downgauging while maintaining pressure resistance for carbonated and functional beverages. The surge in ready-to-drink tea, energy drinks, and sparkling water is reshaping volume demand toward sleek and slim formats.

How is the Opportunistic is the Rise of North America in the Lightweight Aluminum Beverage Cans Industry?

North America is expected to be the fastest-growing region in the lightweight aluminum beverage cans industry due to accelerated contract conversions from plastic and glass to aluminum across carbonated soft drinks, hard seltzers, energy drinks, and ready-to-drink cocktails. Major beverage companies are securing long-term supply agreements with can manufacturers to stabilize input costs and ensure volume availability.

The region’s well-established recycling infrastructure and high scrap recovery rates support increased use of recycled aluminum, helping producers lower carbon intensity while protecting margins.

U.S. Lightweight Aluminum Beverage Cans Market Trends

The U.S. serves as a strategic production and innovation hub in the lightweight aluminum beverage cans industry, supported by highly automated draw-and-iron manufacturing lines that enable advanced metal downgauging without compromising structural integrity. Strong recycling infrastructure and high recycled-content utilization enhance cost efficiency and carbon performance.

Growth is driven by expansion in ready-to-drink beverages, hard seltzers, and energy drinks, alongside sustained capital investments in rolling mills, recycling capacity, and next-generation can-making technologies.

More Insights of Towards Packaging:

- U.S. Glass Packaging Market Size and Segments Outlook (2026–2035)

- Flexible Packaging Adhesive Market Size, Trends and Regional Analysis (2026–2035)

- France Pharmaceutical Packaging Market Size, Trends and Regional Analysis (2026–2035)

- Japan Packaging Machinery Market Size, Trends and Competitive Landscape (2026–2035)

- Repackaging Service Market Size and Segments Outlook (2026–2035)

- Corrugated Automotive Packaging Market Size, Trends and Competitive Landscape (2026–2035)

- Barrier-Coated Flexible Paper Packaging Market Size, Trends and Regional Analysis (2026–2035)

- Bio-Based Packaging Market Size, Trends and Competitive Landscape (2026–2035)

- Active and Intelligent Packaging Market Size and Segments Outlook (2026–2035)

- Plain Packaging Market Size, Trends and Regional Analysis (2026–2035)

- Packaging Waste Management Market Size, Trends and Competitive Landscape (2026–2035)

- Track and Trace Packaging Market Size, Trends and Segments (2026–2035)

- Single-Use Plastic Packaging Market Size, Trends and Competitive Landscape (2026–2035)

- Unbleached Kraft Paperboard Market Size, Trends and Segments (2026–2035)

- Egg Boxes and Trays Market Size and Segments Outlook (2026–2035)

- Corrugated Packaging for Pharmaceutical Market Size, Trends and Competitive Landscape (2026–2035)

- Germany E-Commerce Packaging Market Size and Segments Outlook (2026–2035)

- Corrugated Box Packaging for Electronics Market Size, Trends and Regional Analysis (2026–2035)

- Reusable Cold Chain Packaging Market Size, Trends and Competitive Landscape (2026–2035)

- Polypropylene Corrugated Packaging Market Size, Trends and Competitive Landscape (2026–2035)

Segment Outlook

Type Insights

The standard beverage cans segment dominates the lightweight aluminum beverage cans market because it offers optimal manufacturing efficiency, proven performance, and broad compatibility with existing filling and distribution systems. Its uniform specifications simplify supply chains, minimize tooling costs, and ensure high consumer adoption across carbonated drinks, beer, and ready-to-drink categories. Widespread production capacity and established recycling streams further reinforce its market leadership over niche formats.

The slim/tall beverage cans segment is expected to be the fastest-growing segment because it is widely used in energy drinks, ready-to-drink cocktails, flavoured waters, and functional beverages aimed at younger, urban, and health-conscious consumers. Their sleek shape supports premium branding, portion control, and convenient on-the-go use, while also using less aluminum per unit.

Beverage companies prefer these formats for stronger shelf differentiation and sustainability positioning, which is accelerating demand across premium and lifestyle-focused drink categories.

Wall Gauge Insights

The lightweight cans segment dominates the lightweight aluminum beverage cans market because it delivers immediate material savings, lower production costs, and reduced transportation expenses without sacrificing structural strength. Beverage producers adopt lightweight cans to meet sustainability targets, cut carbon emissions, and improve supply-chain efficiency. Established manufacturing lines and compatibility with existing filling systems further support large-scale adoption across carbonated, alcoholic, and ready-to-drink beverage categories.

The ultra-lightweight cans are expected to be the fastest-growing segment, expanding rapidly as beverage manufacturers intensify efforts to optimize material utilization and protect margins amid aluminum price volatility. Advanced alloy engineering and precision forming technologies now allow further thickness reduction while maintaining structural integrity for carbonated and high-pressure beverages.

These cans enhance freight efficiency, reduce per-unit metal consumption, and support corporate decarbonization commitments, making them increasingly preferred in large-scale beverage production contracts.

Beverage Type Insights

The beer and malt beverages segment dominates the lightweight aluminum beverage cans market due to its high production volumes, strong compatibility with can packaging, and established global consumption patterns. Cans protect flavor, block light exposure, and enable faster cooling, making them ideal for beer distribution. Large brewery contracts, high-speed filling lines, and widespread retail acceptance further reinforce their leading position across both mass and craft beer categories.

The energy & sports drinks are expected to be the fastest growing segment in the market due to rising demand for convenient, on-the-go beverages among younger and fitness-focused consumers. These products are typically sold in slim, lightweight cans that support premium branding, portion control, and rapid chilling. Strong marketing investments, frequent product launches, and expansion into functional and performance drink categories are further accelerating adoption.

End-User Insights

The large global beverage brands segment dominates the lightweight aluminum beverage cans market due to their massive production volumes, long-term supply agreements with can manufacturers, and strong purchasing power. These companies actively invest in lightweighting initiatives to reduce material costs, improve logistics efficiency, and meet sustainability targets. Their global distribution networks and consistent demand ensure stable, high-capacity utilization across can-making facilities.

The craft brewers & small beverage makers segment is the fastest-growing in the market due to increasing consumer preference for premium, artisanal, and limited-edition drinks. Lightweight cans offer flexible production runs, easy branding through digital printing, and convenient packaging for on-the-go consumption. Their smaller-scale operations benefit from lower setup costs, faster time-to-market, and sustainable packaging that appeals to environmentally conscious consumers.

Recent Breakthroughs in the Lightweight Aluminum Beverage Cans Industry

- In December 2025, Canpack US LLC, a packaging company, signed a collaboration with Royal Swinkels, a company, to launch a new version of the 2025 8.6 Tattoo Limited Edition can design. The newly introduced version 2025 8.6 Tattoo Limited Edition continues a long-running tradition of turning the 8.6 Original 50cl beverage can into a canvas for bold artistic expression.

- In August 2025, Novelis, a prominent supplier of sustainable aluminum solutions and a global leader in aluminum rolling and recycling, announced today that it and DRT Holdings, LLC (DRT) have signed a joint development agreement. This agreement is working on hastening the use of alloys with a high recycled content in aluminum beverage can ends.

Top Companies in the Lightweight Aluminum Beverage Cans Market & Their Offerings:

Tier 1:

- Ball Corporation: Produces a wide range of Sleek, Slim, and Standard cans using proprietary alloy technology to significantly reduce container weight.

- Crown Holdings, Inc.: Offers a global portfolio featuring the ultra-lightweight Libra can, which weighs less than 10 grams.

- Ardagh Group: Manufactures optimized 33cl to 50cl cans that reduce aluminum usage by up to 10% through advanced thinning processes.

- CANPACK S.A.: Provides Fit and Slim formats designed for material efficiency and a lower environmental footprint.

- Silgan Containers LLC: Specializes in high-efficiency, sustainable aluminum packaging focused on structural integrity and material reduction.

- Toyo Seikan Group Holdings, Ltd.: Developed the a-TULC technology, creating high-performance lightweight cans that eliminate water-intensive production steps.

- CCL Industries Inc.: Focuses on premium, impact-extruded aluminum containers that combine lightweight design with high recyclability.

- Nampak Ltd.: Supplies the African market with cost-efficient, lightweight aluminum cans tailored for high-volume beverage distribution.

Tier 2:

- Orora Ltd.

- Envases Group

- CPMC Holdings Ltd.

- Kian Joo Can Factory Berhad

- Baosteel Metal Co., Ltd.

- MSCANCO

- Bangkok Can Manufacturing

- Universal Can Corporation

- Showa Denko KK

- Daiwa Can

- GZ Industries

- Can‑One USA

Segment Covered in the Report

By Can Type / Format

- Standard Beverage Cans (330–500 ml)

- Slim / Tall Beverage Cans

- Mini / Small Cans (<250 ml)

- Large Format Cans (>500 ml)

- Retortable / Specialty Cans

By Wall Gauge / Weight Category

- Ultra-Lightweight Cans

- Lightweight Cans

- Conventional / Standard Aluminum Cans

By Beverage Type

- Carbonated Soft Drinks (CSDs)

- Beer & Malt Beverages

- Energy & Sports Drinks

- Juices & Fruit Drinks

- RTD (Ready-to-Drink) Tea & Coffee

- Alcoholic Seltzers / Hard Seltzers

- Functional / Health Drinks

- Other Beverages

By End-User

- Large Global Beverage Brands

- Regional / Local Beverage Producers

- Craft Brewers & Small Beverage Makers

- Private Label / Store Brands

By Region

North America:

- U.S.

- Canada

- Mexico

- Rest of North America

South America:

- Brazil

- Argentina

- Rest of South America

Europe:

- Western Europe

- Germany

- Italy

- France

- Netherlands

- Spain

- Portugal

- Belgium

- Ireland

- UK

- Iceland

- Switzerland

- Poland

- Rest of Western Europe

Eastern Europe

- Austria

- Russia & Belarus

- Türkiye

- Albania

- Rest of Eastern Europe

Asia Pacific:

- China

- Taiwan

- India

- Japan

- Australia and New Zealand,

- ASEAN Countries (Singapore, Malaysia)

- South Korea

- Rest of APAC

MEA:

- GCC Countries

- Saudi Arabia

- United Arab Emirates (UAE)

- Qatar

- Kuwait

- Oman

- Bahrain

- South Africa

- Egypt

- Rest of MEA

Invest in Our Premium Strategic Solution: https://www.towardspackaging.com/checkout/5973

Request Research Report Built Around Your Goals: sales@towardspackaging.com

About Us

Towards Packaging is a global consulting and market intelligence firm specializing in strategic research across key packaging segments including sustainable, flexible, smart, biodegradable, and recycled packaging. We empower businesses with actionable insights, trend analysis, and data-driven strategies. Our experienced consultants use advanced research methodologies to help companies of all sizes navigate market shifts, identify growth opportunities, and stay competitive in the global packaging industry.

Stay Connected with Towards Packaging:

- Find us on Social Platforms: LinkedIn | Twitter | Instagram | Threads

- Subscribe to Our Newsletter: Towards Sustainable Packaging

- Visit Towards Packaging for In-depth Market Insights: Towards Packaging

- Read Our Printed Chronicle: Packaging Web Wire

-

Get ahead of the trends – follow us for exclusive insights and industry updates:

Pinterest | Medium | Tumblr | Hashnode | Bloglovin | LinkedIn – Packaging Web Wire | Globbook | Substack | Bluesky | Justdial | Crunchbase | TrustPilot | Bizcommunity - Contact: APAC: +91 9356 9282 04 | Europe: +44 778 256 0738 | North America: +1 8044 4193 44

Our Trusted Data Partners

Precedence Research | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Healthcare Webwire | Packaging Webwire | Precedence Research Insights

Towards Packaging Releases Its Latest Insight - Check It Out:

Europe Pharmaceutical Packaging Market Size, Trends and Segments (2026–2035)

North America Pharmaceutical Packaging Market Size and Segments Outlook (2026–2035)

Europe Transfer Molded Pulp Packaging Market Size, Trends and Regional Analysis (2026–2035)

Europe Food Packaging Market Size and Segments Outlook (2026–2035)

Shrink Label Films Market Size, Trends and Competitive Landscape (2026–2035)

U.S. Rigid Packaging Market Size, Trends and Segments (2026–2035)

North America Packaging Market Size, Trends and Regional Analysis (2026–2035)

North America Plastic Packaging Market Size, Trends and Segments (2026–2035)

Biopolymer Packaging Market Size, Trends and Segments (2026–2035)

Next-Generation Packaging Market Size, Trends and Competitive Landscape (2026–2035)

Recycled Materials Packaging Solutions Market Size and Segments Outlook (2026–2035)

Commercial Printing Market Size, Trends and Competitive Landscape (2026–2035)

Packaging Films Market Size and Segments Outlook (2026–2035)

Contract Packaging and Fulfilment Services Market Size, Trends and Regional Analysis (2026–2035)

Canada Pharmaceutical Packaging Market Size, Trends and Segments (2026–2035)

South Korea Cosmetic Packaging Market Size, Trends and Competitive Landscape (2026–2035)

Germany Flexible Packaging Market Size, Trends and Competitive Landscape (2026–2035)

U.S. Cosmetic Packaging Market Size, Trends and Competitive Landscape (2026–2035)

U.S. Pharmaceutical Packaging Market Size, Trends and Regional Analysis (2026–2035)

![]()

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.